What Doctors Should Care About in the CARES Act (the Coronavirus Relief Package)

This post may contain links from our sponsors. We provide you with accurate, reliable information. Learn more about how we make money and select our advertising partners.

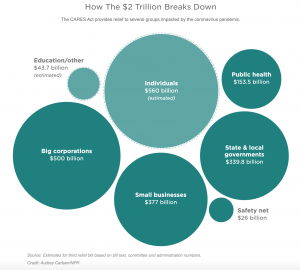

On Friday, March 27th, 2020, Congress passed the Coronavirus Aid Relief and Economic Security (CARES) Act. It’s a $2 trillion bill intended to provide relief to multiple individuals and businesses during the pandemic crisis.

The act is quite huge in scale and so I think it helps to see where the money is allocated visually.

The bill has so many parts to it, you can read it here in its entirety if you want. However, for the purpose of this post, I'm going to stick to the highlights that I think this audience would be interested in or “care” about (see what I did there?).

CPAs are still figuring this whole thing out and I'm in constant communication with mine during this time. So as I get more clarity on these topics, I'll continue to update this post.

*Disclaimer: I am not a tax or financial professional, please consult one before making any decisions on your own personal situation.

Who Is Getting Individual Checks?

You’ve probably all heard of checks the government is sending out. It’s technically an advance on a rebate check for your 2020 taxes, but in essence, it’s free cash. Who doesn't love free money? Some of you will qualify so it's worth looking into.

Here are the major details:

- You will receive a $1200 check as an individual if you have an Adjusted Gross Income (AGI) up to $75,000.

- You will receive a $2400 check if you filed jointly and have an AGI up to $150,000.

- You will receive an additional $500 for each child under 17 if you meet the conditions above.

- There is a phaseout above those totals so you could receive a partial check. For every $1,000 of AGI above those thresholds, you’ll receive $50 less.

- So if you’re single without children and your AGI > $99,000 or a married couple without children and your AGI > $198,000, you will be totally phased out and not receive anything.

- The AGI used to qualify for this is based on 2019 tax returns or if you haven’t filed yet, it’s based on your 2018 returns.

Withdrawing From Retirement Accounts

There are two major changes to note:

1) Withdrawing money from your IRA

You can take an early withdrawal of up to $100,000 from your IRA without the 10% early withdrawal penalty. You’re still responsible for the taxes, taxed at your ordinary income tax rate, but you have 3 years to pay off that tax. So you could spread it out over 2021, 2022, and 2023.

If you want to put the money back, you can do so over the next 3 years which will minimize your tax burden.

2) Accessing money from your 401k, 403b, or 457b

Previously, you could take a loan from your retirement account up to the lesser of $50,000 or 50% of your account balance. That is now increased to the lesser of $100,000 or 100% of your account balance.

You also have three years to pay back the loan without having to pay taxes on it. Previous that window was 60 days.

So depending on how your retirements are structured, you could potentially withdraw up to $200,000 from your retirement accounts if you needed the cash. For a couple, make that amount $400,000, of course assuming you have that in your accounts to begin with.

This benefit is for people who have experienced coronavirus hardship – you got the virus, your family got it, or you were financially impacted by it, which I’m guessing is almost everyone.

Mortgages

If you’re experiencing financial hardship, you can ask your lender for a forbearance on your Federally-backed residential loan. They must grant the request without fees, interest, or penalties for 180 days. There are options to extend it. Banks cannot foreclose for 60 days.

If you're experiencing financial hardship with your Federally-backed multifamily loan, you are eligible for a 30 day forbearance and can be extended for another 60 days under certain conditions. This is key for those landlords out there who are wondering whether tenants will be able to pay rent during this time of economic hardship.

Small Business Loans

Now we get to one of the most interesting part of the CARES Act in my opinion – the various loans and grants available to small business owners and sole proprietors.

Does this apply to doctors?

Yes, if you have your own practice, are an independent contractor. In essence, if you receive a K-1 or 1099, it applies to you.

It can apply to you as an employed doctor with a W-2 if you have a side hustle and get a 1099 from that.

There are two major loans to consider, the SBA Economic Injury Disaster Loan (EIDL) and the Paycheck Protection Program (PPP).

You can also watch this interview & Q/A I had with Toby Mathis, Esq about the different loan options.

Here’s a quick summary of these loans:

The purpose of these loans is essentially to help small businesses maintain their payroll (and not have to lay workers off) and continue to operate thereby preventing a total economic meltdown.

The EIDL loan comes directly from the Small Business Administration, and the PPP loans are from Private Lenders and Banks that have been approved by the SBA.

Deciding which one is better is an individual decision. It totally depends on your cash needs and the size of your payroll. But it’s nice to know that there are options. The first step is to understand what they are and how they differ.

Economic Injury Disaster Loan (EIDL)

You can see the application and apply directly for the EIDL here.

Here are the highlights:

- The loan amount can be up to $2 million.

- Who is eligible:

- Small businesses with < 500 employees

- Private Nonprofits

- Independent Contractors

- Sole Proprietors

- Loan is provided by the SBA directly

- Personal guarantee if loan > $200,000

- Collateral for loans > $25,000

- Interest on loan: 3.75% for businesses, 2.75% for nonprofits

- $10,000 emergency grant (see below)

- Automatic deferral of principal/interest for up to a year

- Can be used for payroll, equipment, rent, and other operating expenses

Emergency Grant

As part of the EIDL, there is an emergency grant potentially available to small business owners in the form of a $10,000 forgivable loan that can be used to pay for immediate operating costs including payroll, fixed debt, accounts payable, sick leave, and more.

First come, first served from what I hear. This will run out quickly.

I'm guessing that sole proprietors and doctors that receive a 1099 like independent contractors and per diem physicians will be running to apply for this if they haven't already.

Paycheck Protection Program (PPP)

Here are the highlights:

- Up to 2.5x average monthly payroll up to $10 million

- Who is eligible:

- Small business < 500 employees

- Independent Contractors

- Sole Proprietors

- Self-employed

- Loan is provided through SBA-approved lender

- No personal guarantee

- No collateral

- Interest: capped at 4%

- Loan forgiveness for 8 weeks of operating costs including: payroll, rent, mortgage interest, starts when the loan is originated

- Automatic deferral of principal/interest payments for 6-12 months.

- Can be used to cover payroll, health care benefits, insurance premiums, mortgage interest, rent, utilities, employee compensation up to $100,000

- Clarification, if you have an employee that makes greater than $100,000, only the first $100,000 can be counted toward the loan usage.

Healthcare

As part of the act, hospitals will $100 billion for hospitals responding to the coronavirus. $11 billion was designated for diagnostics, treatments, and vaccines.

As promised, Telemedicine standards were relaxed. This was necessary especially in this time of social distancing to ensure that patients were being seen. In my opinion, this whole situation has dramatically hastened the eventual replacement of many standard checkups with virtual ones.

$16 billion was also assigned to increase availability of equipment including ventilators and masks as well as for increased hiring. This can't come fast enough for parts of the country that have been hit hard by the coronavirus.

Student Loans

Lastly, let's talk about student loans, which is an area doctors know all too well. All loan and interest payments are deferred through September 30th, 2020 without penalty to the borrower for all federally owned student loans. If you've refinanced with a private lender, unfortunately this doesn't apply to you.

However, I've heard it doesn't hurt to reach out to your private lender if you are truly experiencing economic hardship. If there's ever a time where they'd be lenient on payments, this is it.

So What Can You Do?

Well, the first thing to do is to see if any of the highlights mentioned above applies to you. Then figure out if you can be strategic in utilizing these benefits.

For example, it might make sense to delay your 2019 taxes if your AGI is below the threshold for getting those rebate checks. If your 2019 income instead brings you under the AGI threshold and makes you eligible for those checks, file your 2019 tax return before trying to claim the checks.

If you absolutely need the cash, there are ways to access some from your retirement accounts with paying a penalty. The catch is that most likely you'll have to sell some assets (stocks, mutual funds) to create that cash. Not necessarily the ideal situation since you're giving up on some future tax-protected growth. However, if you've got better use for that cash, then it's actually a good option.

If you're experiencing economic hardship (as I know many physicians are during this time) and truly have difficulty paying your mortgage, consider calling your lender to see if you can receive a forbearance on your loan. You'll still owe that amount eventually so I'd only utilize this if absolutely needed.

Figure out which SBA loan makes the most sense in your situation. There are forgiveness options or essentially grants for both the EIDL and PPP, so see what provides you the most benefit. This will totally differ for the per diem doctor who receives a 1099 vs the physician who owns a practice with a large amount of staff.

Whatever you decide to do, recognize that some of these are time sensitive or budget sensitive (meaning there is only so much money to go around) so you want to figure this out sooner rather than later.

For those who could use a little more assistance, especially those who have a larger payroll, the trusted advisors at Anderson Business Advisors do have an assistance package (hand-holding service) that might interest and make sense for you. This is an affiliate link.

Thank you to all the doctors & healthcare workers who are literally putting your lives at risk to get our families, our society, and our world through this challenging time.

Disclaimer: The topic presented in this article is provided as general information and for educational purposes. It is not a substitute for professional advice. Accordingly, before taking action, consult with your team of professionals.