Top 5 Expenses That Could Go Up in Retirement

This post may contain links from our sponsors. We provide you with accurate, reliable information. Learn more about how we make money and select our advertising partners.

At some point in our careers, we'll come to a point where we decide retirement is near. We've saved, we've prepared, and we've planned for our time out of the regular work-horse routine.

But, while some expenses go down as expected, others go up. Physician on FIRE provides insight into 5.

Today’s Classic is republished from Physician on FIRE. You can see the original here.

Enjoy!

A few weeks ago, I celebrated the Top 5 Expenses That Go Down in Retirement. Every dollar you don’t spend when retired is $25 to $33 you don’t need to set aside for retirement. Drop $10,000 in expenses and your required nest egg is at least a quarter-million dollars smaller. Awesome!

But… there’s a not-so-awesome part.

Some expenses go down, sure. Others will remain roughly the same. Some spending categories, though, can, unfortunately, be expected to go up.

Ay, there’s the rub. Every $1,000 you plan to spend per year requires roughly an extra $25,000 to $33,000 in savings to support it (based on a 3% to 4% withdrawal rate).

As was the case when we looked at costs dropping, none of these will apply to everyone, but it’s a good idea to think about your own expenses and how they might change in retirement. To me, these are some of the top culprits that could bust your budget when you leave the traditional workplace behind.

The Top 5 Expenses That Could Go Up in Retirement

1. Healthcare

For many, health insurance is at least partially paid for by an employer. In retirement, you’re on your own until Medicare kicks in at 65, and even then you’ll probably purchase Medigap insurance and perhaps prescription drug coverage.

As our bodies age, they tend to need more maintenance and repair work. Early retirees can expect to visit a good doctor more often in their fifties and early sixties than they did in their thirties and forties. The insurers and their actuaries know this and price your coverage accordingly.

There may be options to mitigate an otherwise meteoric rise in this line item in your budget. Health sharing ministries have become more popular in recent years, and the purchase of a catastrophic plan is now allowed without an ACA penalty at any age.

If you remain active and healthy and can afford most but not all out-of-pocket costs (think cancer treatment or extended ICU stay), a catastrophic plan could make sense for you.

Nonetheless, we’re budgeting $20,000 a year for healthcare coverage in the short term, understanding that the costs are rising faster than the rate of inflation, and even that number may be inadequate.

2. Travel

What do many people do with their newfound freedom in retirement? Explore the world!

Whereas you may have been confined to one or two quick trips during your working years, you now have the time to roam if you want to. While travel costs will probably drop off eventually, perhaps in your eighties or nineties, you could have decades of saying Yes to trips that you previously said No to because you were working.

Just going part-time, we’ve seen an uptick in our travel costs. We spent three weeks in Mexico not long ago, and we spent a few more weeks in Hawaii. We’ve also been to Honduras twice, and we travel as a family of four. If you start traveling more with kids, the costs can add up quickly!

Again, you may find ways to keep travel costs from completely blowing your budget. You can travel at off-peak times, take advantage of last-minute bargains, and slow travel in a manner that doesn’t cost much more than your normal day-to-day. However, if you’re anything like me, you can expect the travel budget to grow in retirement.

3. Education

Education costs come in many forms. If you’re an early retiree, you may have yet to put your kids through college. If they will go through college after you stop earning an income, you’d better have planned ahead by funding 529 Plans or helping them apply for financial aid.

If you have kids in elementary or high school, you may live in a location where private schools are commonplace and a borderline necessity. Those are some expensive years!

If your children have completed all the paid education they’re ever going to get (or you don’t have children), you may still incur some education expenses in retirement. You may want to learn new skills, and choose to buy some education via community ed, community college, or possibly pursue a full-fledged degree at a university.

With time on your hands, the desire to learn something new may be stronger than ever. You may be able to audit classes for free and get your books at the public library rather than Amazon, but don’t be surprised if your education costs are increased in retirement.

4. Purchases

If idle time leads to in-person or online shopping, your credit card could get a real workout in retirement. Even if you don’t consider yourself to be a shopper, that doesn’t mean you won’t spend more money on stuff when retired.

Maybe you’ll pick up a new hobby.

Photography — gotta get the latest camera body and lenses. Golf — You’ll spend more on the experience and the equipmentHunting and fishing. Did you know that an ice auger and Vexilar can set you back over $1,000 before you cut your first hole in the ice? And this is the kind of fishing that doesn’t even require a boat!

With more time on your hands, you’ll find new things to do. And some of those will undoubtedly cost money — money that you weren’t spending when you were too busy working.

5. Gifts

The rising costs of gifts in retirement can be expected to come in two forms: to other people and to charity.

The older you are, the more relatives you’ll probably have to buy gifts for. As a kid, you probably gave gifts to your parents and siblings. As a young adult, you might have added nephews, nieces, and perhaps children of your own.

As a retiree, you may see your kids have kids. And those kids can have kids (once they’re no longer kids, of course). You could have a large bevy of grandchildren and great-grandchildren. That’s a lot of birthday and Christmas gifts!

As you mature in age and your portfolio matures with it, unless you encounter a particularly poor sequence of returns in the early retirement years, you could find yourself with a portfolio that greatly exceeds your needs.

In fact, according to the Trinity study, the median outcome after 30 years is to nearly triple the money you started with. This is a good problem to have, and you may be inclined to share the wealth, as we have done preemptively with a sizable donor-advised fund.

You’ve probably noticed that most big benefactors of charitable organizations tend to be a lot older than you. Their hard-earned dollars have benefitted from the magic of compound interest, and they are doing some good with the abundance. Perhaps it will be you holding up the oversized check one day.

The Retirement Smile

We’ve talked about expenses that are likely to drop in retirement:

- cost of commuting

- retirement savings

- taxes

- mortgage

- raising children

- professional clothing

Now, we’ve touched on expenses that could rise in retirement:

- healthcare

- travel

- education

- purchases

- gifts

What’s an aspiring future retiree to do?

First, understand that your future expenses will probably not be the same as they are now. Whether your future life will cost more, less, or about the same depends on the stage in life you’re currently in, and how the above factors or others will affect you personally.

Of course, it’s impossible to guesstimate your future spending if you don’t know your current spending, so it’s important to have an idea of what that looks like. I used to have a rough idea, but after I started a blog, I decided to track our spending more closely. In 2016, we spent about $62,000 and in subsequent years, that number didn’t change much.

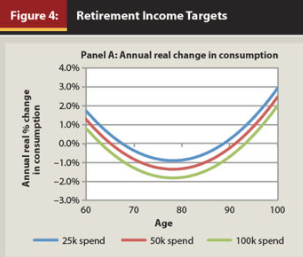

It also helps to recognize the “retirement smile.” It’s not the sly grin you’ll be wearing on weekdays when most of the people you know are clocked in — well, it could be — but I’m talking about the spending pattern that most people will see in retirement.

Wade Pfau, Ph.D., CFA, the Retirement Research, explains it well in this post based on David Blanchett’s work at Morningstar. The average retiree can expect to see expenses drop in the years after retiring at 65, and the trend typically continues downward until the early 80s when healthcare spending begins to rise.

The resulting downslope followed by an upslope gives you a sort of “smile” when plotted along a timeline. At some point, there just isn’t much more you want to purchase.

You may run out of places you’re excited to explore or lack the energy and physical capacity to do so. Eventually, the cost of nursing homes, procedures, and hospital stay more than makeup for the difference if you make it to that stage of life.

This post begins and ends with the cost of healthcare. I suppose that’s appropriate.

What expenses do you foresee rising when you retire? Any or all of the above? Do you have a number 6?

To subscribe to new posts and get access to an amazing free spreadsheet, please consider subscribing to the site. It’s free and POF promises not to spam you.

Join our community at Passive Income Docs Facebook Group. Just click below…

Disclaimer: The topic presented in this article is provided as general information and for educational purposes. It is not a substitute for professional advice. Accordingly, before taking action, consult with your team of professionals.