Why I’m Beginning My Retirement Today… In My Thirties

This post may contain links from our sponsors. We provide you with accurate, reliable information. Learn more about how we make money and select our advertising partners.

I’m a firm believer in a gradual or phased retirement. We’ve all heard the advice: “Start saving for your retirement now, and hopefully by the time you’re 60 or 65, you’ll have built up enough of a nest egg to quit working.”

It almost seems as if we’re being told to just grind it out for 30 years, all in the hopes that you can actually enjoy the 30 years after that. Is that what life’s really about?

I have two kids under the age of three. Do I really want to wait until they’re 30 to be able to enjoy spending time with them? The reality is that by then, they’ll have their own lives and possibly, families of their own. That just doesn’t sit well with me.

That’s why I’ve worked to set myself up in a way that allows me to start cutting back now, and begin enjoying a little bit more of life. Life itself is unpredictable; just look online and you’ll see that tragedies are occurring more and more frequently with each passing day. My fellow physicians, life is short. Are we spending it living only for the future, or can we start enjoying it now? Surely a better balance exists.

That’s why I’ve worked to set myself up in a way that allows me to start cutting back now, and begin enjoying a little bit more of life. Life itself is unpredictable; just look online and you’ll see that tragedies are occurring more and more frequently with each passing day. My fellow physicians, life is short. Are we spending it living only for the future, or can we start enjoying it now? Surely a better balance exists.

Now, I don’t necessarily advocate quitting your day job just to enjoy the present. On the contrary; I enjoy being a doctor and I hope I can continue working in some capacity for a very long time.

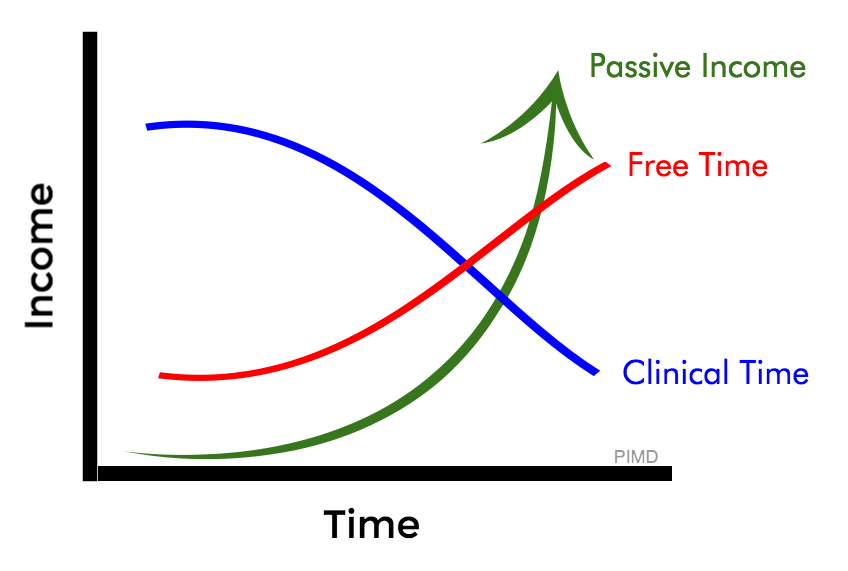

How is this possible? Well, it works if you can exchange some of your current daily income with passive income. As this income grows, you can, in a sense, begin your retirement now. Through my different ventures and depending on the month, a good chunk of my expenses are covered entirely by passive income.

Sure, there will be unexpected things that come up and I know there are some huge expenses headed my way (newsflash: putting your kids through school is expensive!). But hopefully, the streams of passive income I’ve set up will take the edge off some of those expenses.

I realize doing this for yourself can be a real test of willpower. It feels quite unnatural because as physicians, we’re used to working up to the breaking point. We consider idle time wasted, and if we give up a shift or case, we focus only on the money we could have made if we had worked.

I realize doing this for yourself can be a real test of willpower. It feels quite unnatural because as physicians, we’re used to working up to the breaking point. We consider idle time wasted, and if we give up a shift or case, we focus only on the money we could have made if we had worked.

We tend to forget what we gain in return: time spent with family and time to recharge our batteries. You can’t put a price on these things. Seeing the joy on my daughter’s face as we play in the pool – that’s the kind of thing I’ll remember when I’m older, not the shift I gave up last week.

We tend to forget what we gain in return…

There are many articles out there that examine the top regrets of the dying. Almost universally, people’s biggest regrets are working too hard, and they wish they had spent more time with their loved ones. Not a single person regretted not having more money, a better car, or a bigger house. That’s a powerful lesson, and it’s one that I want to learn and live by.

This idea of “early” retirement is obviously not something you can attempt to do without a plan. Fortunately, I have one and have been working hard to implement it.

So I’m going to give up my shift this weekend to a hungry colleague, and I’m going to begin my retirement… today.

Has anyone else begun to try this, or perhaps are considering it for yourself? Let me know your experiences; I’d love to hear them!

Disclaimer: The topic presented in this article is provided as general information and for educational purposes. It is not a substitute for professional advice. Accordingly, before taking action, consult with your team of professionals.